Post 1Q26: Attractive combination of growth and profitability

1Q26 largely in line, small model updates

1Q26 was a solid start to the year, with Eurobank on track to deliver on its plan and upside to both NII and net fees guidance for FY16, in our view. With small model changes, we arrive at adj. EPS of 43cps for FY26E (+14% yoy), ROTE of 16.7% (vs. management target of ~16%) on a CET1 of 14.3% (our revised forecasts are within). We see the ROTE reaching ~18% by FY28E vs. management guidance of ~17%, as we see some upside to the plan. We remain Buy rated, with an unchanged PT of €4.70/share.

SEE quarterly earnings progression subdued, but poised to grow

As shown within, SEE earnings have been relatively subdued over the last few quarters (Figure 2), although NII has started to inflect upwards (Figure 3), with SEE NIM at 2.77% also higher than Greece at 2.23% (Figure 5). A VES was implemented in Cyprus, reducing headcount by 200, while operational integration of the two banks in Cyprus is expected in early 2027. Bulgaria’s adoption of the Euro in January is expected to boost loan growth, while Eurobank is also benefiting from lower reserve requirements (NII tailwind of €20m pa). SEE loan growth has been solid at 8.5% yoy, with the plan indicating double digit growth expectations in the medium-term (UBSe 11% pa FY25-28E).

See upside to NII and net fees guidance

The results showed solid growth of NII (+4% yoy, 2.6% qoq) with robust growth in both performing loans (+9.8% yoy) and investment securities (+23% yoy), combined with a stable NIM. We see upside to NII guidance of ~€2.6bn for FY26E (UBSe €2.79bn). Net fees (+20% yoy in Q1) surprised positively, with continued strong growth of its asset management business, as well as lending fees. We see upside to guidance of fees growth of ~10.5% pa over the next three years to FY28 (UBSe 13% pa), including a contribution from Eurolife (included from August 2026 onwards). The Euroflie acquisition will consume about 120bps of CET1 (before considering the Danish compromise), still leaving the CET1 ratio above 14% by year-end (UBSe 14.3%).

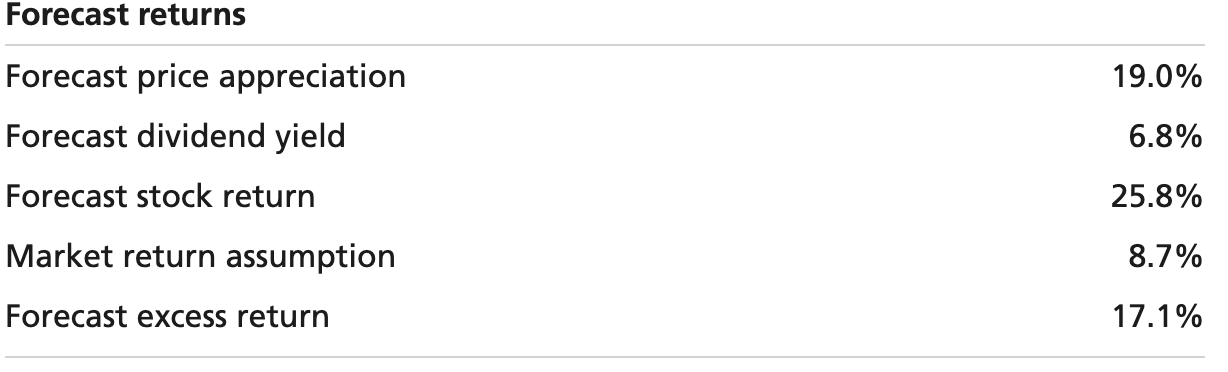

Valuation: 1.5x TNAV vs. ROTE of 16.7% (FY26E)

Our unchanged PT of €4.70/share is based on a two-stage capital adjusted GG model, assuming a sustainable ROTE of 18%, COE 11%. The shares are on a FY26E PE of 9.3x, a 10% discount vs. European banks (10.3x), and on a FY27E PE of 8.2x, 8% discount to European banks (9.0x). The dividend yield of ~7% (FY27E) is attractive, while buybacks (~40% of FY25 distribution, UBSe 20% of FY26E) support EPS growth.