Post 1Q26: Upgrade EPS, factoring in bancassurance

Model updates, incorporating Allianz bancassurance agreement

1Q26 beat mainly on exceptional trading revenue, although NII (+2% qoq) also beat and is running ahead of plan on robust loan growth (+12% yoy). We factor in the announced intention to enter into a bancassurance arrangement with Allianz, which we forecast would boost fee growth to ~12% pa FY25-FY28E (vs. our previous forecast of 9% pa). We also incorporate the impact of a lower headcount following the VES. We therefore upgrade adj. EPS by ~5-6% over the next three years, as we see an EPS CAGR of 10% pa. We forecast the ROTE to land at 17.4% by FY28E on a CET1 of 15.3%, indicating an underlying ROTE on a normalised CET1 (13.5%) of 19.2% by then.

Attractive opportunity in bancassurance

With a large retail client franchise, NBG is punching below its weight in insurance, in our view, generating only ~€17m pa in fee income. The announced exclusive bancassurance agreement with Allianz, including taking a 30% stake in Allianz Greece, should lift its bancassurance fees by ~4x as we factor in €65m pa by FY28E (ramping up over time). We therefore upgrade our average net fees growth for FY27 & FY28 to 13.8% pa from 8% pa before, which results in a 3-year CAGR of ~12% pa (FY25-FY28E). With Allianz providing expertise, products and technology, we see minimal incremental investment required to deliver this net revenue uplift. The transaction is guided to be ~4% EPS and 50bps ROTE accretive, coming with a capital cost of only 20bps.

Front loaded opex and optimisation, to deliver medium-term benefits

FY26 is a year of elevated cost growth (UBSe +8% yoy) as it invests in the franchise and completes its core banking transformation, while we model cost growth to subside towards a 3-year CAGR of 6% pa (FY25-FY28E). With a sizeable VES implemented in Q1 at a cost of €60m, the headcount is expected to fall by 280 or ~4.2% this year (already reduced by 227 in Q1), per company guidance, driving lower staff cost growth going forward, but also upskilling and re-energising the workforce.

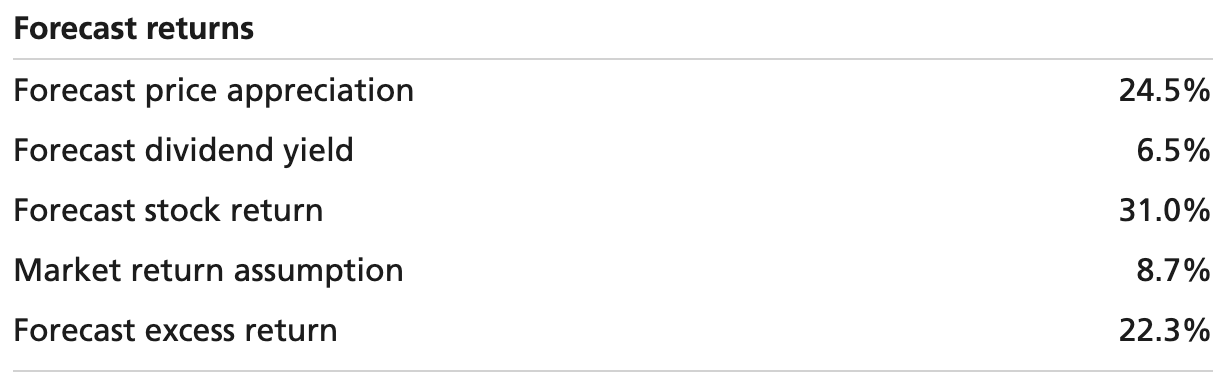

Valuation: 1.5x TNAV vs. FY26E ROTE of 15.3%, sustainable ROTE of 18.5%

Our two-stage capital adjusted Gordon growth derived price target increases by 4% to €18.20. The shares are relatively highly rated on a P/TNAV of 1.5x, FY26E PE of 9.8x (FY26E), although still at a slight discount to European banks on 10.3x, offering among the highest ROTE (adjusting for excess capital) in Europe. We see potential for continued high distributions as we factor in a normal payout of 60% and special distributions of €150m in FY26E and FY27E, while the CET1 still lands at 15.3% by FY28E, indicating further potential to raise distributions.