Solid 1Q26, remains a top pick

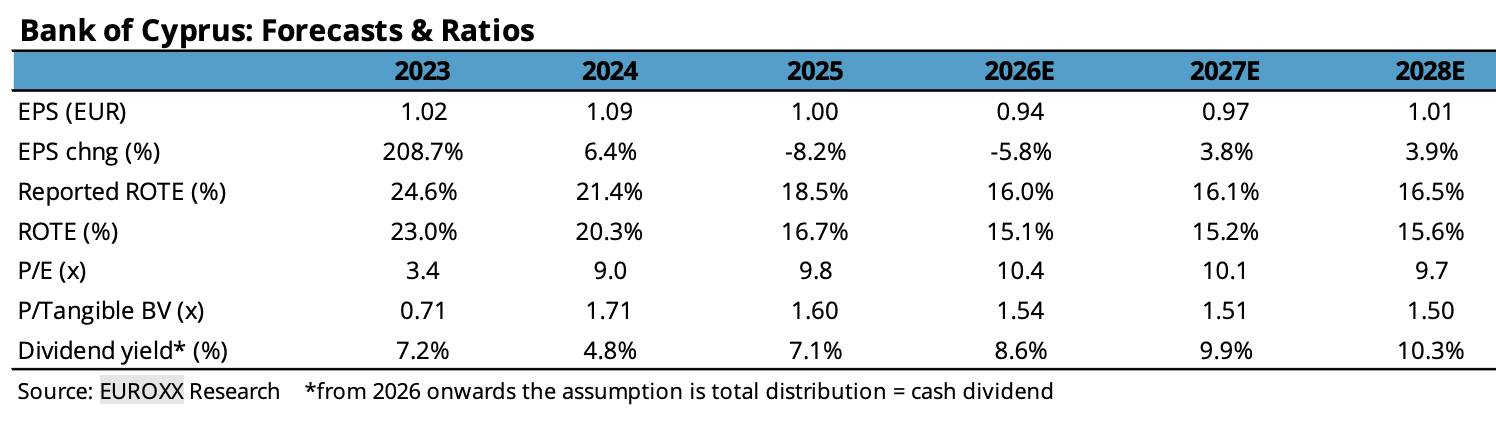

Bank of Cyprus reported a strong start for 2026E with high lending growth, supportive NII and fees and a low cost of risk. Management reiterated the target for mid-teens reported ROTE in 2026E or >20% on a min 15% CET1 with 1Q26 trending at 18.0% and 26.5% respectively. In view of the solid first quarter, we see an upside risk in the 2026E management targets and our estimates. We remain buyers on Bank of Cyprus with the shares trading on a P/E in 2026E similar to European peers but with a superior dividend yields and capital.

A good start despite the geological concerns: Bank of Cyprus reported1Q26 net profits of EUR 121m, ahead of our estimate of EUR 112m mainly due to a provision reversal for a specific large customer. On an underlying basis, the results are driven by strong lending growth (+2% qoq and 8% yoy) and higher fixed income portfolio (+5% qoq), offsetting the lower calendar days in 1Q26. All other key P&L items came in line with our forecasts besides the impairment line (with the reversal more than offsetting the revised macro assumption). The CET1 ratio stood at 20.3% (from 21.0% at year-end 2025), due to the the negative impact from the CBD transaction (35bps) with organic capital generation at 114bps.

Upgrades ahead likely: Management re-iterated the financial targets for2026E (NII at c.EUR 720m, >5.0% loan growth, c.40% C/I ratio, 40-50bpsCOR and mid-teens reported ROTE) but we do see an upside risk on theback of solid loan growth, potentially higher rates and provisions below the low end of the range guided by management (40-50bps). We are alsovery confident and see an upside risk in our net profit forecast for 2026E(reported at EUR 435m) in view of the first quarter run rate. This will implydistribution yields in excess of 8.5% per annum for 2026-28E, with an evenhigher level if current estimates prove conservative.