CITI’S TAKE

Interest rates are pricing in potential rate hikes premised on the Fed needing to cool an overheating economy, but data have us increasingly convinced that upside risks to inflation are limited. Real incomes are flat to down and will not drive the type of consumer demand that allows firms to raise prices. The June FOMC meeting may feature the removal of the easing bias and “dots” showing no cuts this year. Still, we expect a combination of lower oil prices, dovish messaging from Chair Warsh, and softer jobs data to lead markets to price-out hikes and price-in cuts over the next few months.

Data on incomes and consumer spending will not substantially change the economic outlook for Fed officials or markets. The economy is expanding, unemployment has been stable around 4.3-4.5% and inflation is running above , but a substantial slowdown in real incomes suggest a softening outlook for consumer demand that increases downside risk to growth and makes sustained consumer inflation unlikely.

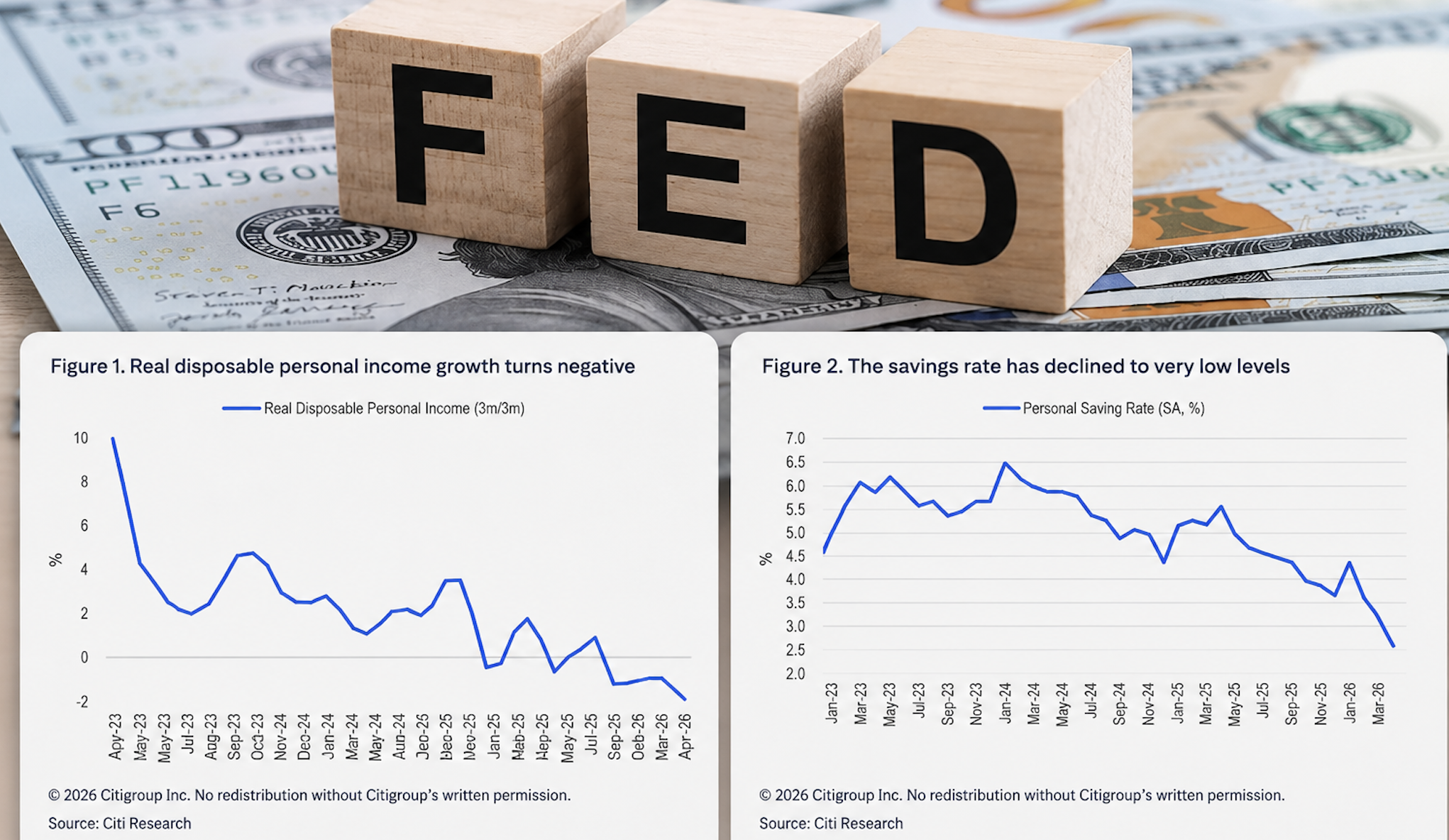

Consumer spending has slowed from closer to 3% annualized to a still respectable 2% rate, but real incomes have slowed more dramatically and have been flat to declining in recent months. (Disposable real income is down just over 1%YoY but would be closer to flat if not for volatility in farm subsidies.) That is not typical of an expanding economy and not a stable equilibrium. So long as consumer spending continues to outstrip income growth, the savings rate will keep declining – and it already is at an historic low.

At 2.6%, the rate is around those observed in the years just prior to the 2008 financial crisis. A low savings rate will not in and of itself cause an economic slowdown, but it does present a downside risk to economic growth if a shock to consumer confidence (e.g., a rise in unemployment or decline in equity prices) were to rapidly push desired savings back to a more normal range.

The savings rate has also been low in recent years only to be revised higher in annual revisions. We think it is less likely that there will be large upward revisions to income this year, as immigration and population growth have slowed substantially (previous underestimation of income could have been due to large population inflows that were difficult to capture in initial estimates).

Consumer spending is now slightly softer in the rearview, with Q1 real consumer spending revised down to 1.4%QoQ from 1.6%QoQ. Real GDP was revised from 2.0%QoQ to 1.6%QoQ due to the downgrade to consumption and weaker inventory investment.

To the extent consumer spending continues to slow, the US economy will become even more reliant on AI investment as a source of growth. This tailwind continues to blow strongly and is driving expansion in the industrial sector and broad-based strength in durable orders. Core PCE inflation registered 0.24%MoM and 3.3%YoY in April, close to expectations. The reading was boosted by the BLS “making up” for recording zero shelter inflation during the government shutdown last October by recording double the rate of shelter inflation in April. Without this “catch-up,” monthly core PCE would have been closer to target pace at just below 0.20%MoM. Shelter inflation has slowed this year as expected and continued weakness in house prices and rents suggest shelter will remain a disinflationary force.

Non-shelter core services or “supercore” inflation has stayed stubbornly elevated in both core CPI and PCE. Part of the strength in PCE has been in portfolio management fees – a category that rises and falls with equity prices. In the April reading, PCE supercore was just 0.12%MoM – but that reflected the equity sell-off in March and will likely rebound in the May inflation reading.

Core goods inflation was projected to soften as tariff pass-through would be complete. This has largely occurred in core CPI goods, but core PCE goods has been elevated due a surge in computer memory prices that is (inappropriately) magnified in PCE relative to CPI. This methodologically driven differential between core PCE and core CPI is becoming more widely understood with former Fed Governor Miren and coauthors publishing a paper documenting the issue last week. This may ultimately form part of an argument for treating core PCE as less reflective of broader trends in consumer prices with more attention paid to trimmed-mean or other alternative inflation metrics.

We believe it is too early to see pass-through from higher energy prices to stronger goods prices, but evidence so far suggests this pass-through will be limited. One of the fastest to react prices should have been airfares, but the rise in domestic airfares in recent months has not been outsized relative to expectations assuming unchanged jet fuel prices, and international airfares have actually declined as demand has softened.

Data released this week make us more convinced that the combination of soft incomes and weak hiring will prevent persistent consumer inflation from taking hold, but Fed officials will not have shifted from their on-hold stance, seeing a stable unemployment rate, an economy that is still expanding, and above-target inflation. At the June FOMC meeting, we would expect a significant upward revision of core inflation, a median “dot” showing no cuts (instead of one) this year and statement language that removes the “easing bias.”

Still, we see three dovish dynamics that are likely to play out over the second half of the year and have interest rate markets pricing-out potential hikes and pricing-in cuts.

1.Reopening of the Strait of Hormuz resulting in lower oil and gasoline prices.

2.“Residual seasonality” leading to softer labor market data in coming months.

3.Dovish messaging from Fed Chair Warsh with a focus on alternative, cooler inflation metrics and the idea that AI investment now – even if it boosts some prices – will lead to disinflation later.

It may take a couple months for these catalysts to materialize. While we see risk of a softer jobs report next week, our base case is for solid 60k payrolls and a stable 4.3% unemployment rate. Stable low initial and continuing jobless claims and the last two months of above 100k payrolls mean it will probably take multiple months of data for Fed officials to be pushed dovish by labor market developments.