About 100 BlackRock portfolio managers and executives gather at our biannual Investment Forum this week as a world shaped by supply accelerates. Speed and scarcity are defining how mega forces intersect. The AI buildout and Mideast conflict spur questions about financing, energy security and interest rates as strong AI-driven earnings offset higher rates. Yet questions persist over valuations and the ultimate AI winners. These debates will shape our Midyear Outlook.

The investment landscape is being reshaped by a world shaped by supply – and mega forces are increasingly intersecting and driving investment opportunities. This is the overarching theme at our Midyear Investment Forum. The AI buildout’s planned capital spending – already historic at the start of the year – has only accelerated. Mega cap hyperscaler investment estimates have soared in just two quarters, with projected annual spending now approaching $1 trillion by 2028. See the chart. This is testing the constraints we laid out in our 2026 Global Outlook. First, hyperscalers are financing the buildout via increased debt issuance as rates reprice higher, in line with our leveraging up theme this year. The AI buildout’s big power needs for data centers show where the AI theme crosses with the energy transition. And constraints are increasing from political opposition to data centers.

The massive AI buildout has seen our Outlook’s micro is macro theme unfold. But big questions remain about how the AI theme will play out. At the company level, is AI adoption translating into greater profit margins or revenues – or is token usage for complex tasks eroding other gains? Will AI investments pay off and justify valuations – and who will capture the value? AI is already creating winners and losers – so what comes next for disrupted software companies? This comes as a growing pipeline of big AI-related IPOs— such as SpaceX, OpenAI, and Anthropic — will likely increase competition for capital.

A strengthening AI mega force

The AI theme has driven U.S. and some regional stocks to all-time highs, even as bond yields and energy prices have jumped due to the Middle East conflict and resulting disruptions to energy flows and supply chains. That’s because AI-driven earnings growth has proved strong enough to help offset the drag from higher interest rates. But disruption to the Strait of Hormuz is exposing the global economy’s dependence on critical energy flows: the longer the closure persists, the greater the risk of a broader supply shock – with a bigger hit seen to Europe and Asia. This reinforces how the mega forces we track are increasingly intersecting, as AI-driven demand collides with geopolitical fragmentation. These tensions will be central to debates at this week’s Forum bringing together about 100 of BlackRock’s portfolio managers and investment executives.

The jump in bond yields this year highlights how traditional portfolio ballast is less reliable — reinforcing our diversification mirage theme and the need for a more dynamic, whole portfolio approach to investing. That’s why we see a greater role for active returns, with hedge funds and private markets as portfolio diversifiers in this environment. How mega forces are forcing a rethink of the role of portfolio diversifiers – and portfolio construction itself – will be another key topic of debate. On a tactical basis, our overweight to U.S. stocks has worked out so far this year – and we were quick to dial up risk after the outbreak of the Middle East conflict. We have stayed underweight long-term U.S. Treasuries – and 10-year yields are near one-year highs. The outlook for interest rates will also be a key debate. The Midyear Forum helps us kick the tires on our tactical views for the second half of the year and refresh our investment themes for our Midyear Outlook on June 30.

Our bottom line

Mega forces are shaping the investment environment – and the debate at our Midyear Forum. We stay overweight U.S. equities on the AI theme and resilient earnings but will stress test our tactical views.

Market backdrop

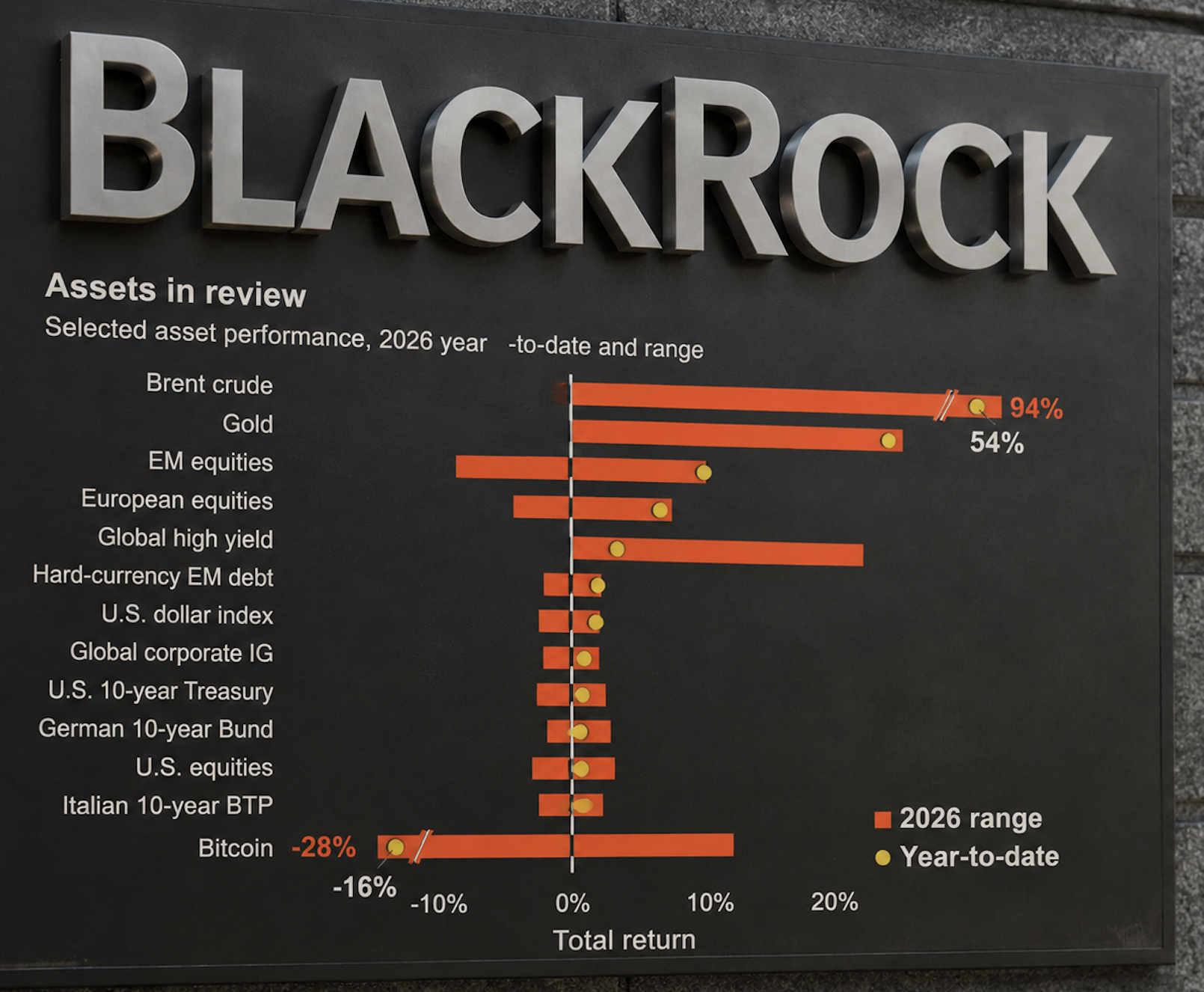

Reports of a deal between the U.S. and Iran – including a reopening of the Strait of Hormuz – drove Brent crude oil prices down 11% this week to near $92 a barrel. The S&P 500 hit new record highs, led by semiconductor stocks on strong earnings tied to AI demand. The Philadelphia Semiconductor Index rose 5% this week and has gained in eight of the past nine weeks. U.S. Treasury yields pulled back from recent one-year highs, with the 10-year yield falling 14 basis points to near 4.43%.

Markets this week will focus on U.S. labor data, with April job openings and May payrolls testing whether the recent hiring strength is holding up. Payroll growth is seen modest but stable, reinforcing the view of a still-resilient labor market and keeping the Fed focused on sticky inflation. ISM surveys are expected to show ongoing growth, though higher energy costs from Middle East disruptions could slow momentum.

Tracking five mega forces

Mega forces are big, structural changes that affect investing now – and far into the future. They change the longterm growth and inflation outlook and are poised to create big shifts in profitability across economies and sectors. This creates major opportunities – and risks – for investors. See our web hub for our research.

- Demographic divergence: The world is split between aging advanced economies and younger emerging markets – with different implications.

- Digital disruption and artificial intelligence (AI): Technologies are transforming how we live and work.

- Geopolitical fragmentation and economic competition: Globalization is being rewired as the world splits into competing blocs.

- Future of finance: A fast-evolving financial architecture is changing how households and companies use cash, borrow, transact and seek returns.

- Transition to a low-carbon economy: The transition is set to spur a massive capital reallocation as energy systems are rewired.