Q2/H1 likely to beat and FY EBIT guidance raised; Solid story, but we see better value in Beer

CITI’S TAKE

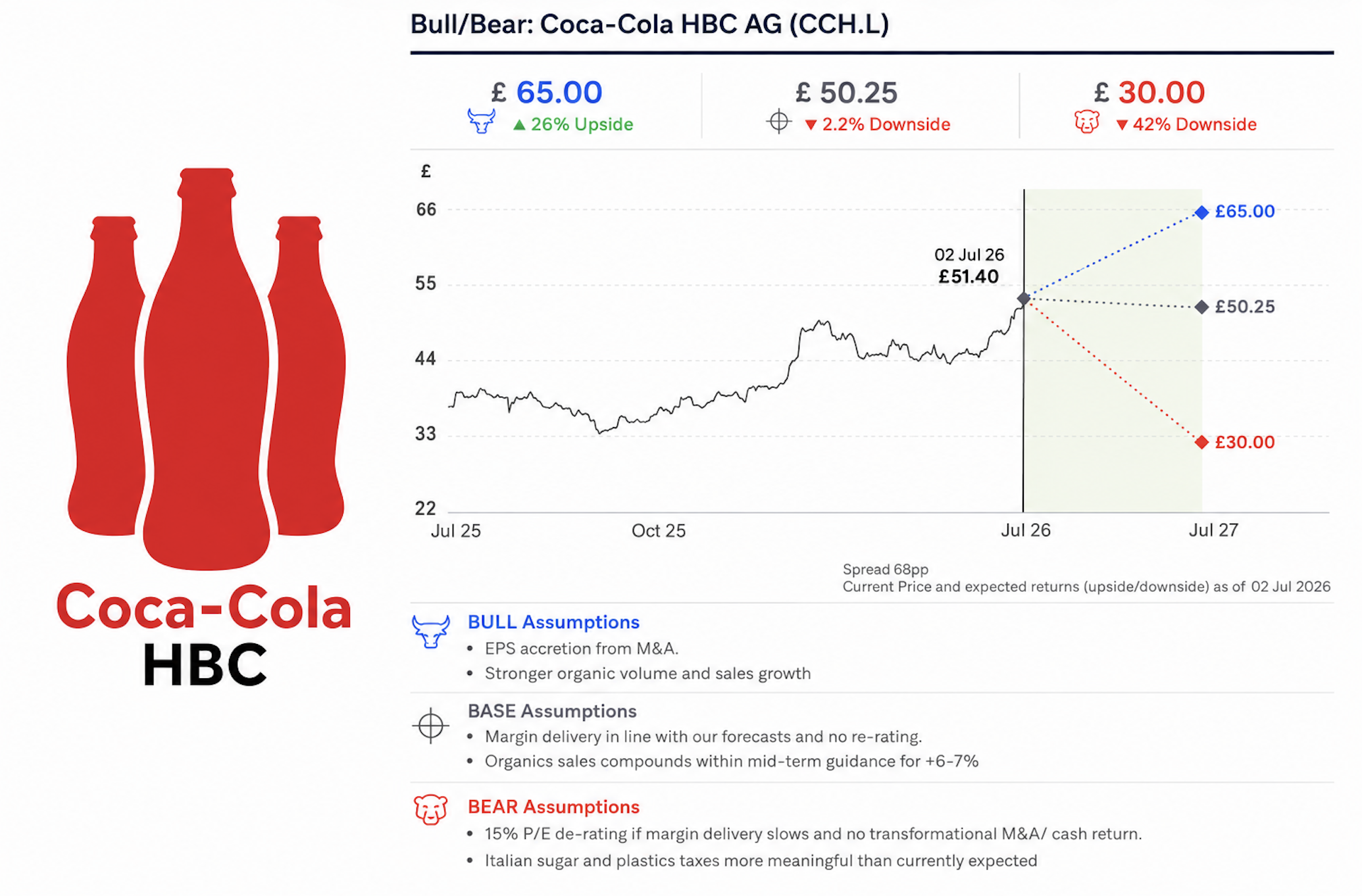

Favorable Q2 weather and a delay in implementation of Greece’s DRS system means we expect Q2/H1 results to beat consensus expectations and CCH to raise FY26E organic EBIT growth guidance with its August 6th results. We forecast Q2 organic volumes +3.9% and OSG +6.5%, c.+80bps ahead of consensus. This means we now anticipate H1 organic EBIT +13.4% (cons. +11.3%). With H1 profit delivery H1 skewed and if July European weather remains favorable, we expect management to raise FY26E organic EBIT growth guidance to +9% to +11% with the H1 print. Despite on-going positive earnings momentum, and further earnings accretion from the completion of the CCBA transaction in H2 26E, the group’s full valuation (PE c.20x) and still significant exposure to Russia, means we prefer Beer stocks Carlsberg, ABInBev, and Heineken. We increase our target price to £50.25.

Q2 delivery on track; June/early July trading likely to be supportive — CCH will report Q2/H1 26E results on 6 Aug. We expect the favorable Q2 weather, and a particularly good June, coupled with the postponement of Greece’s DRS rollout to Q4 to drive higher than expected volume in the period. We upgrade our Q2 26E organic volume growth estimate by +30bps to 3.9% in this report (consensus 3.1%). However, we note the period includes the last time impact from the group’s decision to prioritize profitable waters in Italy (c.-250bps to the market, -100bps to Established Markets and -20bps to group). We forecast Q2 OSG +6.5% (cons. 5.9%).

H1 delivery Organic EBIT delivery H1 skewed. We estimate organic EBIT +13.4% — Overall H1 organic growth is being supported by Q1’s 4 extra selling days. We expect H1 organic volumes to be +6.5% and OSG at 8.8%. The slightly better Q2 topline momentum than we previously anticipated means we now estimate H1 organic EBIT growth of +13.4%, (previously 12.5%) and ahead of consensus at +11.3%.

FY26E organic EBIT growth guidance likely to be raised to +9% to +11% — Given: 1) likely better Q2 trading; 2) a skew of organic EBIT growth delivery to H1; and 3) if Q3 European weather remains favourable, we expect management raise FY26E organic EBIT growth guidance. We expect CCH to guide for FY26E OSG of +6% to +7and organic EBIT 9% to 11% (prior 7%-10%). We forecast FY26E organic volumes +3.5%, (previously +3.3%, Cons. +2.9%) OSG of +5.9% (previously +5.7%, Cons. +5.8%) and organic EBIT growth of +10.0% (previously +9.6%, Cons. +9.2%).

We upgrade our EPS estimates by +1-2% and target price to £50.25 – The combination of small upgrades to our organic estimates and the marking-to-market for current FX prompts a +1.2% upgrade to FY26E EPS and +1.7% to FY27E. These changes and the roll forward our DCF increase our price target to £50.25.

Established Markets – For Established Markets, we forecast Q2 26E organic volumes up +1.5% (VA cons +0.5%), as the Easter phasing unwind is offset by better weather and a delay in implementation of Greece’s DRS to Q4. In Italy, we model volume decline of -1% as the group continuous to face impact of water withdrawal while for Switzerland we model +5% given easy comps. We model +3% organic volumes in Ireland while for Greece, we forecast volume +2%. We model FX-n value/case growth of +1.5% to leave Q2 organic sales growth of +3.1% (VA cons +2.2%).

Developing Markets – For Developing Markets, we model organic volume growth of +2.1% (VA cons +1.6%) for Q2-26. In Poland, we model organic volumes up +2% given DRS implementation effective from Oct-25. In Hungary, we model organic volume growth of +2% on tough comps while in Czech Republic, we model volume growth of +3% on easy comps. For the region, we model Q2 FX-n rev/case growth of +3.3%. Overall, we model Q2 organic sales growth of +5.4% (VA cons +5.0%).

Emerging Markets mix – In Emerging Markets, we model organic volume growth of +5.2% (VA cons +4.2%). In Romania, we model volumes down -2% given challenging environment and low consumer confidence due to political instability. In Nigeria, we model +7% organic volume growth as the group is performing well in more stable macro environment. For Egypt, we model organic volume growth of +12%. In Russia, we model volume growth of +5% while Ukraine remains tricky (Citi -3%) but the market is at least recovering from recent supply chain disruptions. Overall, we model divisional FX-n rev/case growth of +4.0% and Q2 organic sales growth of +9.4% (VA cons +9.3%).