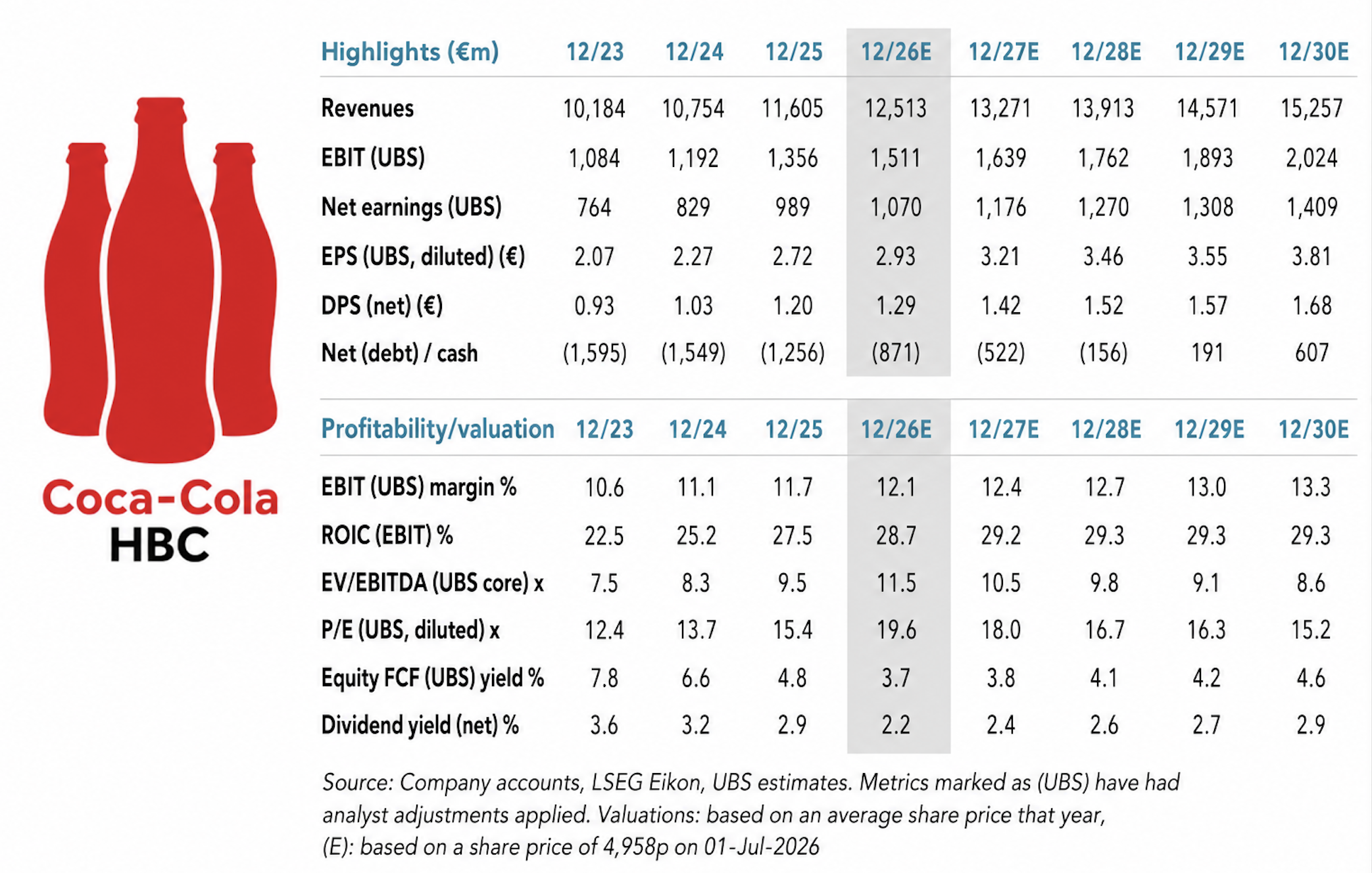

Q2/H1 26 results preview: Upside on Q2 volumes and H1 EBIT

Upside on Q2 volumes: We forecast Q2 organic revenue +7.2%, ahead of VA consensus +5.9%, with upside on volumes (UBSe +4.3% v cons +3.1%) in all regions. We also expect upside to H1 organic EBIT (UBSe 13.8% v cons +11.3%), which reflects management prior comments that profit growth is likely H1 weighted. We expect this to reassure investors on the FY guidance of 6-7% organic revenue (consensus +5.8%), noting Q1 was below this on a selling day adjusted basis (UBSe +3.5%). We raise FY27 EPS estimates by +2% mainly reflecting recent FX moves, and increase our price target to £56 (from £50), which is based on an EV/NOPAT multiple on CCH ex Russia in line with CCEP, and Russia valued at c50% of our scenario analysis.

Q2/H1 26 results preview – upside on volume in all regions: CCH is due to report Q2/H1 results on 12th August. We forecast Q2 organic revenue +7.2% (cons +5.9%), with volumes +4.3% (cons +3.1%) and price/mix +2.8% (cons +2.7%). Across the regions, we highlight;1) Established (UBSe +1.3% vols vs cons +0.5%): We expect Italy to be held back by a continued 2.5pp headwinds from delisting of water portfolio, however the core CSD portfolio appears strong noting recent Nielsen data (+5.6% in Q2TD vs Q1 +4.1% ) and share gains after a soft Q1. However, we expect solid growth in the rest of the region noting easier comparatives in Austria (lapping prior year DRS implementation); Switzerland (customer dispute) and Greece (later start of summer season in Q2 25); 2) Developing (UBSe +2.8% vols vs cons +1.6%): We expect underlying volumes to accelerate, as Poland stabilises following the headwind from DRS implementation in Q1, and we expect solid growth from Czech (consistent with Q1), and Slovakia is lapping prior year headwinds from sugar tax.3) Emerging (UBSe +5.8% vols vs cons +4.2%): We expect no change in solid underlying trends across Nigeria and Egypt since the Middle East conflict in recent months; Serbia will be supported by the full ramp-up of Bambi production and Ukraine supply chain headwinds likely normalise following disruption in recent quarters, however this is partially offset by weakness in Romania exacerbated by political instability.

EBIT margin: we expect H1 org. EBIT margin to expand +50bps in organic terms (cons as +40bps), driving overall org. EBIT growth +13.8% (vs cons +11.3%) following same H1 skewed FY26 sales pattern given extra selling days in Q1. Our H1 EBIT/EPS estimates are +4/+2% v consensus.

Valuation: CCH trades on a 18x 2027E PE / c18x EV/NOPAT, +11%/+1% premium to average European Staples. We estimate the current share price implies a c10x multiple on Russia (v 0x after the conflict began), assuming CCH ex-Russia trades on c23x EV NOPAT, in line with peer CCEP.

CCH is due to report Q2 26 earnings on 12th August. We forecast Q2 organic volume/revenue +4.3/+7.2%, ahead of consensus +3.1%/+5.9%, with upside in all key regions.

- Established Markets (UBSe Q2 org. vol/sales +1.3/3.4% vs VA +0.5%/+2.2%): We expect underlying volumes +LSD% with improving trends in sparkling in Italy (CSD +5.6% in Q2TD vs Q1 +4.1% per Nielsen – link) and share gains after a soft Q1 partially offset by rationalisation of unprofitable water volume which we estimate to be a c2.5pp headwind); We also note Austria and Switzerland lapping easier comparatives in prior year with DRS implementation as well as Greece given later start of summer season in Q2 25. We expect price/mix to be +2% vs cons +1.6% accelerating vs Q1 which was held back by higher share of larger pack formats and promotion in the previous quarter ahead of Easter season.

- Developing Markets (UBSe Q2 org. vol/sales +2.8%/+6.9% vs VA +1.6%/+5%): We expect selling day adjusted volumes to accelerate, as Poland stabilises following the Q1 disruption from DRS implementation, and no major change in trend across other markets, which solid continuation from Czech and Slovakia which is lapping prior year sugar tax implementation. We forecast price/mix to improve sequentially to +4% (v Q1 +2.7%).

- Emerging Markets (UBSe Q2 org. vol/sales +5.8%/+9.9% vs VA +4.2%/+9.3%): We expect no change in solid underlying trends across Nigeria and Egypt since the Middle East conflict in recent months; Serbia will be supported by the full ramp-up of Bambi production and Ukraine supply chain headwinds likely normalise following disruption in recent quarters, however this is partially offset by weakness in Romania exacerbated by political instability. We forecast price/mix at +3.9% reflecting normalising inflation and market conditions in Nigeria and Egypt.

- EBIT margin: we expect H1 org. EBIT margin to expand +50bps in organic terms (cons as +40bps). This drives overall org. EBIT growth +13.8% (vs cons +11.3%) following same H1 skewed FY26 sales pattern given extra selling days in Q1 to reverse in Q4.